Singapore’s Central Provident Fund (CPF) is certainly in the news these days.

The buzz began with recent announcements made on the rise in the CPF Minimum Sum, our President’s address on the review of CPF at the opening of Parliament, a series of blog posts by a certain blogger, and the accompanying lawsuit of the blogger by the Prime Minister. As you’d imagine, lots of bloggers have weighed in on both the positive and negative aspects of CPF (you can find a tonne of them in SG Daily here). The latest is a blog post clarifying what CPF is on The Ministry of Manpower’s blog, followed by assurances that the Government is looking to enhance the CPF Life annuity scheme.

To gather feedback on CPF, Young NTUC recently organised a focus group discussion on the role of CPF in retirement planning. Invited to participate, I found the session pretty insightful, revealing the thoughts, concerns and wishes of CPF members.

Before I go into that, however, it may be useful for us to do a quick recap of what CPF is.

CPF Contributions and Accounts

Started on 1 July 1955 (yep, even before Singapore became independent), CPF is a compulsory social security plan that assists workers to fund their retirement, healthcare, and housing needs. Each month, employees contribute 20% of their monthly gross salary to the scheme. This is topped up by another 16% by employers subject to certain salary caps and ceilings.

The monthly contributions goes into three different accounts in CPF, namely:

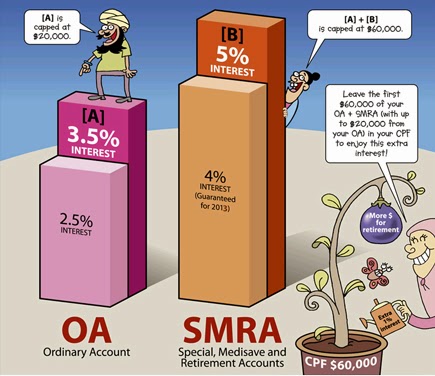

1) Ordinary Account (OA) – where savings can be used to buy a home, pay for CPF insurance, investments and education (both the individual or his/her children). Funds left in the OA will continue to generate a risk-free annual return of 2.5%, with an additional 1% for the first $60,000.

2) Special Account (SA) – where savings are more specifically targeted for retirement and investment in retirement-related financial products. Funds in the SA generate an annual risk-free return of 4%. There is a good article on why you should leave your money in the SA untouched here.

3) Medisave Account – where savings can be used for hospitalisation expenses and approved medical insurance (eg Medishield).

This can be visualised by the picture below (courtesy of CPF):

Courtesy of CPF

What Happens When You Retire?

When you reach 55 years of age, whatever savings you have in SA, followed by OA will be transferred to a Retirement Account (RA) to meet your Minimum Sum (MS).

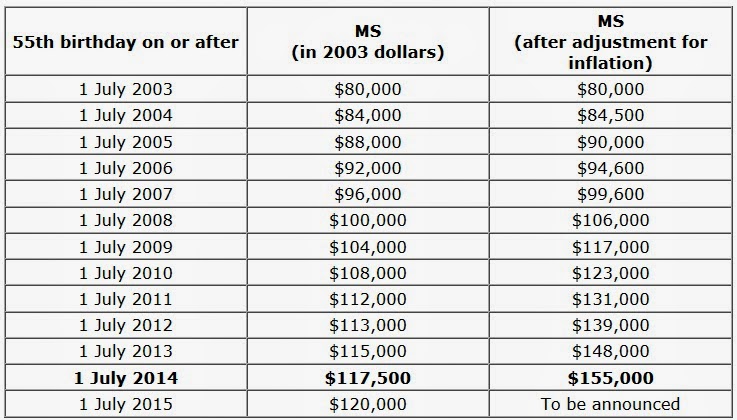

Set at $80,000 in 2003, the MS will be raised gradually to keep up with inflation until it reaches $120,000 (in 2003 dollars) in 2015. This will be raised to $155,000 with effect from 1 July 2014 (see table below).

Courtesy of CPF

So what happens to your retirement funds in the RA? Well, there are two options available:

CPF LIFE

If you leave your CPF retirement funds untouched, you will be eligible for the CPF Lifelong Income For the Elderly or CPF LIFE. This will only kick in if you have at least $40,000 in your Retirement Account when you reach 55 years of age, or $60,000 when you reach your Draw Down Age (DDA). The DDA is currently 63, and is set to increase to 64 in 2015 and 65 in 2018 to keep pace with rising life expectancies (in case you do not know, we are no. 4 in the world).

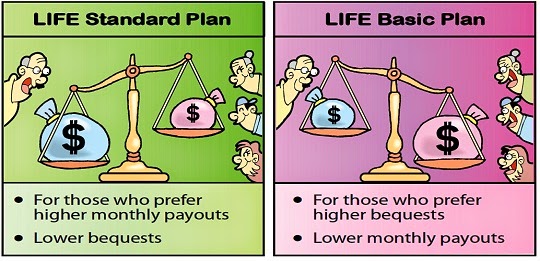

CPF LIFE is an annuity scheme which provides fixed monthly payments until death. You can apply for the LIFE Standard Plan which provides higher monthly payouts and a lower lump sum at the end (when you…err… shuffle off the mortal coil), or LIFE Basic Plan which provides lower monthly payouts and higher bequests (see below).

Courtesy of CPF

To calculate the payoff rates for either plays, you can use the CPF LIFE Payout Estimator. Its quite easy to use actually so give it a spin! I have worked out an imaginary scenario (below) to give you an idea of what the quantums may be like:

From CPF LIFE Payout Estimator

Insurance-Linked Life Annuities

Beyond CPF, you can use the sum to purchase other life annuities from insurance companies like NTUC Income and Great Eastern Life. What these do is to provide insurance cover above and beyond the monthly payouts and the bequests. Naturally, there are many different permutations, and I strongly suggest that you do your research to find out which best fits your needs.

(You can read more about the pros and cons of different forms of life annuities in the following articles from Smart Investor, The Straits Times, and The Edge.)

Now that we’ve got some of the basics out of the way, let us dive into the dialogue proper.

Transparency in Fund Usage

One of the key issues highlighted by participants was the transparency in how CPF funds are invested. Like most laymen, participants were unaware of where the money goes to, or how it generates the return given back to CPF members. This isn’t unique to the participants. Blog posts have been written about how the funds are parked with risky investments by Temasek Holdings or GIC, and these were refuted by the Government.

Quoting from the Government website Factually:

“Our CPF funds are invested in risk-free Special Singapore Government Securities (SSGSs). The returns on SSGSs are pegged to the returns of other bonds in the market with similar risks. There is no connection between GIC’s rate of return and the interest paid on our CPF accounts. GIC invests our foreign reserves in stocks, bonds, real estate and other assets that carry higher risks than SSGSs. The value of SSGS is assured, as they are guaranteed by one of the few remaining triple-A credit-rated governments in the world.”

Despite these clarifications, some are still unclear about where CPF monies are invested in. Of course, while it may be useful for the Government to reveal more information about what exactly the SSGSs are (it isn’t openly traded in the Singapore market), it probably also needs to balance disclosure with our country’s strategic interests.

Flexibility in Draw Down Age

The other issue raised was the draw down age. Could greater flexibility be provided here?

Currently pegged at 63 years of age, this will increase incrementally over the next few years. While most participants agreed that we are living longer – hence the need for greater coverage beyond our retirement years – some felt that the Government should give more prerogative to citizens to decide when they want to use the money.

One suggestion was that instead of ringfencing CPF funds till one hits the draw down age of 63, 64 or 65, the Government could release them in time blocks. This will give members more flexibility in deciding how their funds should be used at an earlier age rather compel them to keep them there.

To circumvent earlier draw down dates by CPF members, incentives could also be put in place to encourage members to park their money there. These should be voluntary rather than compulsory.

Minimum Sum and Inflation

Another issue raised by participants was the minimum sum. If it were to be raised to keep pace with inflation, would it then grow to $200,000 in another 5 to 10 years time? Would there be a cap to this amount? How does the minimum sum compare to the cost of living given current rates of inflation?

While some agreed that the minimum sum should be updated to reflect current realities, others felt that it could be done away with altogether. Those in favour opined that Singaporeans should be mature and educated enough on their own to know how they could plan for their own retirement without undue intervention from the Government. Unfortunately, this approach may result in some Singaporeans falling through the cracks.

Perhaps this quote shared by Young NTUC best reflect the conundrum faced:

“The fact remains that people have a right to spend themselves into bankruptcy. The question is whether the government has a right to allow those people to starve to death.”

Boosting Public Education

Another key issue raised was the need for citizens to gain more access to easily understood information and data. Knowing the whats and hows isn’t enough as often, it is the whys which people are keen to know about. Some of the questions asked include the following:

1) How is the minimum sum established?

2) How is the quantum for the increase derived?

3) What is the average age of Singaporeans and how long do we live?

4) What are the spending patterns like for Singaporeans?

5) What would happen if we cannot hit the minimum sums in our OA, SA and Medisave accounts?

6) Under CPF LIFE, is it better to give away more money as bequests or would it be better to have a higher monthly payout?

7) Why should we buy annuities rather than other financial products?

8) Were there social problem cases before and after the minimum sum?

Honestly, a rather comprehensive amount of information is already provided on the CPF website. For a start, you can dig through some general information on CPF, and make use of the numerous calculators available to compute literally anything, including planning for retirement. There are also tonnes of tips on the IM$avvy website helping you to plan for your financial future.

Having said that, there are definitely fresh opportunities to educate citizens on how they can better manage their CPF funds. These may be especially useful for the less financially savvy or educated folks in the population.

Providing More Options

Participants also favoured granting CPF members more choices in how their funds are used. By doing so, the Government could then cater to the different life trajectories, financial situations, and preferences of CPF holders.

A different set of rules could apply to those faced with terminal/ grave illnesses or financial hardships who needed quicker and easier access to their CPF funds. While the minimum sum ensured that most Singaporeans could meet their monthly living expenses, it could also be a tough hurdle for low wage workers or the cash-strapped to cross.

Finally, more investment options could be granted for retirees beyond the annuities currently provided. Naturally, these could range from the more conservative but less risky options to the higher income but riskier options. Ultimately, CPF holders should have the autonomy to make his or her own informed choices.

Adapting Policies to Suit Different Segments

Last but not least, participants felt that the Government should perhaps conduct a survey to determine what the financial literacy of the population is like. This should cover different age groups. By doing so, we are then better able to decide which groups require more hand holding, while others could be granted more freedom to decide how their funds should be used.

This requires a shift in mindset – one where the Government could place greater trust in the citizens so that they could be empowered to manage their own money. Of course, doing so may also open a Pandora’s Box. The challenge therein lies in balancing between empowering citizens to make the right choices while ensuring that an adequate safety net is provided to the majority.

A Good Scheme Which Needs To Be Updated

Despite their varied views on the CPF, participants were mostly supportive of the programme. While some felt that greater transparency and flexibility is preferred, the general consensus seemed to be that the CPF has played and will continue to play an important role in the retirement needs of the majority of Singaporeans.

What are your views on CPF? Should there be greater flexibility in how it is administered? Do share your views on the REACH website.